a hybrid AI

autonomous

trading system.

Advance Quantitative Research, Innovative Technology, and Institutional-Grade Risk Management

- Act IQuant's Windowthe view

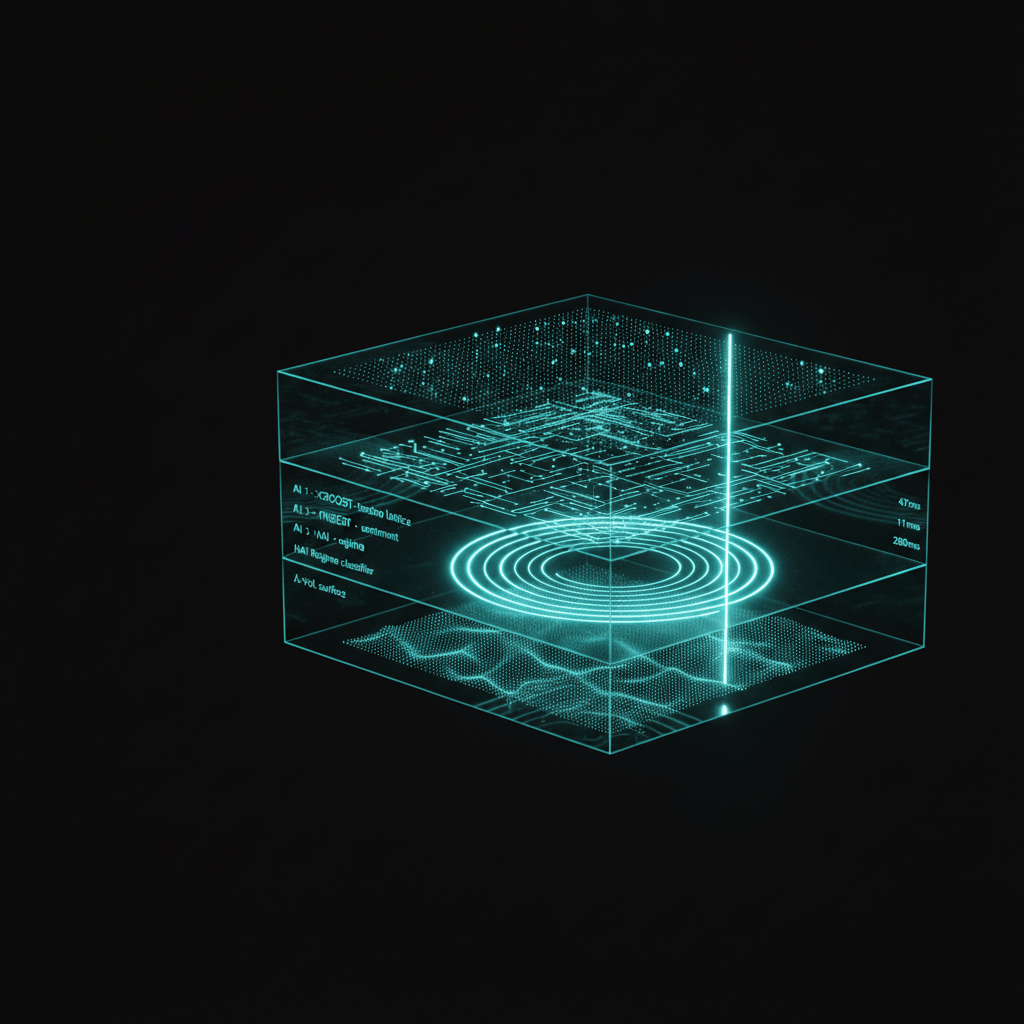

- Act IISeven AI Layersthe gates

- Act IIIAlgorithmic Cathedralthe discipline

- Act IVThe Bridgethe custody

- Act VTrading Floorthe supervisor

Five acts. Editorial pacing. Each anchored by a cinematic still and a single thesis. Scroll down — the program reveals itself in the order an allocator would ask the questions.

you've been trading without the supervisor.

After a combined fifty years inside institutional risk and finance — examining banks at the federal level, advising the largest G-SIBs through their hardest regulatory moments, building capital-markets and model-validation frameworks at trillion-dollar institutions — the gap was always the same. The discipline that protects institutional capital was never available to individual traders. Quant7 is what fixing that gap looks like.

seven AI layers. every trade clears all seven.

Direction-conditional gradient-boosted prediction. Financial-domain sentiment classification on real-time news, filings, and regulatory feeds. Twenty-day rolling regime detection per asset. Volatility-PDE intelligence decomposing variance into regime, feedback, and dissipation. A graph-learned cross-asset network-momentum matrix detecting lead-lag fractures. Cont-style order-flow microstructure mapping bid–ask–cancel imbalance to mid-price drift. Path-signature geometry encoding the order of moves and the signed area between price-volume channels. A signal enters production only after all seven agree — and the deterministic risk gates clear.

- AI 1

- xgboost · 22-feat · dir-cond

- AI 2

- finbert sentiment gate

- AI 3

- HAI regime · 20-day

- AI 4

- λ-vol PDE · L/S/C KL

- AI 5

- network momentum · graph

- AI 6

- OFI microstructure

- AI 7

- path signature · L=2/3

calibrated. not extrapolated.

Seven systems. One hundred twelve independently calibrated configurations. Thirty thousand-plus independently optimized parameters across the system. Each configuration calibrated per asset, per timeframe, per regime by the q7_precision pipeline — Gaussian-Process Bayesian Optimization, Combinatorial Purged Cross-Validation with fifteen out-of-sample paths, Deflated Sharpe statistical floor, Probabilistic Sharpe confirmation, Adaptive Conformal Inference for live drift correction. No black box. The SR 11-7 model-risk framework you'd find inside a G-SIB, applied end-to-end at the level of a single retail subscription.

- systems

- 7

- configurations

- 112

- parameters

- 30,000+

- audit framework

- SR 11-7

seven systems. seven markets.

Each system carries twenty-five calibrated subsystems drawn from a common pool — confluence scoring, regime classification, circuit breakers, ratchet exits, ζ-Field decomposition, and the rest. The asymmetry isn't in the count; it's in which subsystems activate. S7 AVA, trading binary outcomes on prediction markets, substitutes Event-CV Splitting for asset × timeframe CPCV and skips network-momentum, signature features, Λ-Vol KL decomposition, and DTW leader detection.

S7 AVA — AI-Augmented Volatility Arbitrage on prediction markets. Polymarket + Kalshi venue connectors, event-graph CV, binary-outcome PnL accounting. Calibrates around event boundaries — election outcomes, sports, economic surprises — instead of bar timeframes. see the S7 detail page →

algorithmic trading carries substantial risk of loss. past performance does not guarantee future results. Quant7 Alpha, LLC does not custody client assets, does not provide personalized investment advice, and is not a registered investment advisor.

a different shape of market.

a different shape of model.

S1-S6 trade continuous price series. S7 AVA trades binary outcomes — questions that resolve to 0 or 1. Did the Fed hike? Did the NFL game go over? Did Bitcoin close above forty-thousand on the deadline? The underlying mechanics are different enough that S7 carries its own engine taxonomy, its own CV protocol, and its own subsystem specialty within the common twenty-five-subsystem stack.

not TRND / BRK / MR / SWP.

S7 substitutes the four S1-S6 engines with a five-engine taxonomy adapted to event-driven order books and dual-venue CLOBs.

- E1LAT_ARBlatency arbitrage · cross-venue tick race

- E2MM_REBATEmarket-making · maker-rebate harvesting

- E3CROSS_VENUEpolymarket ↔ kalshi spread + funding capture

- E4INTRA_ARBsingle-venue YES/NO mispricing intraday

- E5NEWS_NLPFinBERT-tier NLP on real-time event newswires

no 4 × 4 grid. event boundaries instead.

S1-S6 enumerate 4 assets × 4 timeframes. S7 enumerates heterogeneous markets that resolve on event boundaries — ten crypto-binary + six event-driven.

your capital stays with you.

Always. The platform connects to your brokerage by trade-scope-only API keys — never withdrawal. Keys are AES-GCM encrypted at rest and never logged. The platform never holds funds. Period. You fund your own account, you keep your own custody, the system places trades through your credentials. We are the model. You are the bank.

- scope

- trade-only

- withdrawal

- never

- encryption

- AES-GCM

- platform custody

- zero

the system halts itself before drawdown earns its way to your account.

An agent-governance layer watches every position, every fill, every drift signal. Sixteen specialized agents run continuously — calibration, live execution, risk, governance — each with a charter, each auditable, each accountable to you via permanent decision-log entries. The Adaptive Repair Loop runs two parallel branches off every live trade: a drift branch (Drift Detector → HAI re-trainer) and a structural branch (Code Auditor → Code Repair). Both feed the same learning loop. The discipline doesn't take the night off.

- agents

- 16 · charter §1 user-supreme

- repair loop

- dual-branch · drift + structural

- audit

- permanent decision log

- SDC taxonomy

- 10-class · SDC-01..10

the papers

Every claim has a paper behind it.

A formal architecture paper for each of the seven strategies — edge thesis, the four engines, the order-flow leverage model, the risk stack, the hybrid-AI gate — plus the methodology paper that governs them all: how every parameter is proven before it touches capital. Read the thesis and design of any paper in full; subscribers read the complete papers on-site.v1.0 · June 30 2026

the discipline that protects institutional capital,

finally available to you.

Replace chance with intelligence.

The system is operated by Quant7 Alpha, LLC. SR 11-7 model-risk framework applied end-to-end. Self-custody by design. Trade-scope API keys only. AES-GCM encrypted at rest. Subscriptions billed monthly · cancel anytime.